A compliance risk assessment is the systematic evaluation of risks that could cause regulatory breaches, financial loss, or reputational damage within a financial institution. Known formally as a compliance risk analysis, it identifies where your organization is exposed to legal and regulatory violations, then prioritizes those exposures for action. Regulatory bodies including BaFin, the European Banking Authority (EBA), and standards like MaRisk AT 4.4.2 treat this process as a governance requirement, not an optional audit exercise. For currency exchange operators and financial businesses managing multiple branches, the stakes are direct: penalties can reach €15 million in severe cases, and reputational damage compounds the financial cost.

What is compliance risk assessment and why does it matter?

A compliance risk assessment is defined as a structured, cyclical process that identifies, evaluates, and prioritizes the legal and regulatory risks an institution faces. The word "cyclical" matters. Compliance assessments are dynamic processes that adapt to regulatory changes, business model shifts, and control performance feedback. They are not static annual reports filed and forgotten.

The importance of compliance assessment goes beyond avoiding fines. Institutions that run effective assessments allocate resources to the highest-priority risks instead of spreading compliance budgets thin across every conceivable exposure. That focus produces better controls, cleaner audits, and a stronger regulatory position. A compliance risk analysis also gives your management board a clear picture of where the institution stands, which is exactly what regulators expect to see documented.

One common misconception is that compliance risk assessment is purely a legal task. It is not. Compliance risk assessment is a core governance tool tied to institutional risk appetite and sits within the second line of defense. That framing changes how you staff it, how you report it, and how seriously your board treats it.

What are the essential steps in the risk assessment process?

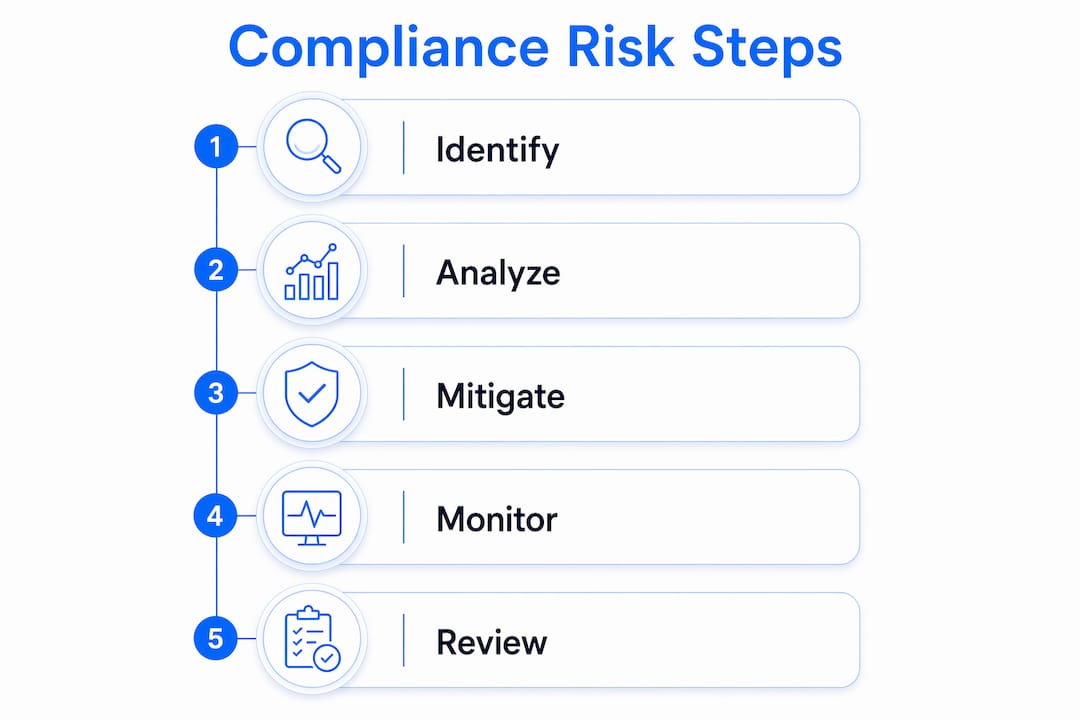

The core compliance risk assessment process consists of four steps: identification, analysis and evaluation, mitigation strategy development, and continuous monitoring. Each step builds on the last, and skipping any one of them produces gaps that regulators will find.

Step 1: Risk identification. Map every area where your business touches a regulatory obligation. Use structured methods: regulatory checklists, process walkthroughs, interviews with business line owners, and review of past audit findings. For a currency exchange operator, this means covering AML obligations, KYC procedures, GDPR data handling, and transaction reporting requirements.

Step 2: Risk analysis and evaluation. For each identified risk, assess two dimensions: likelihood of occurrence and potential impact. A risk that is highly likely but low impact ranks differently than one that is unlikely but catastrophic. This step produces a ranked list, not just a catalog.

Step 3: Mitigation strategy development. Assign controls to each prioritized risk. Controls can be preventive (blocking a violation before it occurs) or detective (catching it after the fact). Document the control owner, the control frequency, and the expected residual risk after the control is applied.

Step 4: Continuous monitoring and review. Controls degrade over time. Staff turn over, systems change, and regulations evolve. Schedule regular reviews of control effectiveness, and trigger ad hoc reviews whenever a material change occurs in your business or regulatory environment.

Pro Tip: Build your identification step around regulatory checklists specific to your jurisdiction. Generic checklists miss jurisdiction-specific obligations. For exchange offices operating under BaFin supervision, MaRisk AT 4.4.2 provides the baseline framework.

Which regulatory standards govern compliance risk assessments?

MaRisk AT 4.4.2 and EBA Guidelines require financial institutions to conduct compliance risk assessments at minimum once per year, plus additional event-triggered updates after material operational or regulatory changes. That dual requirement, annual plus ad hoc, is the standard your compliance program must meet.

Key regulatory frameworks shaping compliance risk governance include:

- MaRisk AT 4.4.2: The German Minimum Requirements for Risk Management mandate documented compliance risk assessments with defined scope, methodology, and reporting lines. The 9th MaRisk amendment tightened the integration requirement between Compliance and Risk Controlling.

- EBA Internal Governance Guidelines: The European Banking Authority's guidelines require institutions to maintain a compliance function with clear risk assessment responsibilities, independent reporting to the management body, and documented findings.

- BaFin supervisory expectations: BaFin expects compliance risk assessments to reflect the institution's actual risk profile, not a theoretical one. Assessors who copy prior-year reports without substantive review face supervisory criticism.

- GDPR and MiFID II: Both frameworks carry their own risk assessment obligations that feed into the broader compliance risk analysis. GDPR requires data protection impact assessments for high-risk processing activities. MiFID II requires ongoing suitability and conduct risk reviews.

Failing to meet these standards carries consequences beyond fines. Regulatory enforcement actions can trigger operational restrictions, mandatory remediation programs, and public disclosure requirements. The reputational damage from a public enforcement action often exceeds the direct financial penalty.

How to integrate compliance risk assessments into business risk management

Compliance risk assessment produces the most value when it connects to your institution's overall risk management framework rather than running as a separate compliance department exercise. The 9th MaRisk amendment explicitly mandates close coordination between the Compliance function and Risk Controlling to integrate compliance risk into the full business risk picture.

Practical integration means three things. First, compliance risk appetite statements must align with the institution's broader risk appetite framework. If your institution has a low tolerance for operational risk, your compliance risk thresholds should reflect that. Second, compliance risk findings must feed into the institution's risk reporting cycle, not just the compliance department's internal reports. Third, the compliance function must have a seat at the table when new products, markets, or processes are being designed.

Pro Tip: Board-level reporting should focus on residual risk and strategic priorities, not technical detail. Overly lengthy audit reports reduce usability; distill your findings into a one-page summary that shows the top five risks, their current control status, and any open remediation actions.

Avoid two common pitfalls. The first is siloed compliance work where the compliance team runs its assessment in isolation and then hands a report to management with no follow-up mechanism. The second is purely legalistic framing, where the assessment reads as a legal opinion rather than a risk management tool. Both approaches produce reports that sit on shelves rather than driving decisions.

You can track how well your compliance controls are actually performing by reviewing activity logs in compliance systems, which provide the operational evidence your assessment needs to be credible.

What are common compliance risks in financial services?

Common compliance risks in financial services fall into several categories, each with distinct regulatory exposure and potential penalties.

- AML deficiencies. Failures in anti-money laundering controls, including inadequate customer due diligence, transaction monitoring gaps, and late suspicious activity reporting. For exchange offices, AML compliance is the single highest-priority risk category given the cash-intensive nature of the business.

- GDPR breaches. Unauthorized data access, inadequate consent management, or failure to honor data subject rights. Penalties under GDPR can reach €20 million or 4% of global annual turnover, whichever is higher.

- MiFID II failures. Suitability assessment gaps, best execution failures, or inadequate product governance documentation. These risks are most acute for institutions offering investment products alongside currency services.

- Transaction reporting errors. Inaccurate or late regulatory reporting under frameworks like EMIR or national transaction reporting regimes.

Risk matrices categorizing risks as critical, high, medium, or low by likelihood and impact are the standard tool for prioritizing these exposures. A critical risk, one with high likelihood and high impact, requires immediate remediation and monthly monitoring. A medium risk can follow a quarterly review cycle with documented controls in place.

Review cycles should match risk severity. Critical risks warrant monthly control testing. High risks need quarterly review. Medium and low risks can follow annual cycles unless a trigger event occurs. This tiered approach focuses your compliance team's time where it matters most.

Key Takeaways

A compliance risk assessment is a governance-critical process that financial institutions must run at minimum annually, integrating findings directly into enterprise risk management and board reporting.

| Point | Details |

|---|---|

| Annual minimum frequency | MaRisk AT 4.4.2 and EBA Guidelines require yearly assessments plus event-triggered updates after material changes. |

| Four-step process | Identification, analysis, mitigation, and monitoring form the core cycle that must repeat continuously. |

| Governance tool, not legal task | Compliance risk assessment belongs in the second line of defense and ties directly to institutional risk appetite. |

| Prioritize with risk matrices | Rate each risk by likelihood and impact to allocate controls and review cycles to the highest exposures first. |

| Board reporting must be concise | Distill findings into residual risk summaries; detailed technical reports reduce leadership usability and slow decisions. |

Why most compliance assessments fail before they start

The most common failure I see is treating the compliance risk assessment as a documentation exercise rather than a decision-making tool. Teams spend weeks producing detailed reports, then file them without linking findings to any operational change. The assessment looks complete on paper, but nothing in the business actually changes.

Effectiveness depends on actionable outcomes regularly verified by internal audits to confirm controls work beyond their theoretical design. That sentence should be printed above every compliance officer's desk. A control that exists in a policy document but has never been tested is not a control. It is a liability.

The second failure is disconnection from the business. Compliance officers who run assessments without input from operations, technology, and product teams produce risk inventories that miss the actual exposures. The best assessments I have seen involve business line owners in the identification step, not just the compliance team reviewing documents in isolation.

The third failure is reporting complexity. Leadership needs to make decisions, not read compliance textbooks. When your board report runs to 80 pages of technical findings, the critical risks get buried. Institutions that integrate compliance risk assessments effectively gain competitive advantages through better resource allocation and regulatory positioning. That advantage only materializes when leadership actually understands and acts on the findings.

Start with a one-page residual risk summary. Add the full technical detail as an appendix for those who need it. That structure respects your board's time and gets the right decisions made faster.

— Bartas

How Currexchanger supports compliance risk management

Running a compliance risk assessment across multiple exchange offices requires consistent data, reliable transaction records, and audit-ready documentation at every branch.

Currexchanger is built for exactly that operating model. The platform provides AML/KYC compliance tools, real-time transaction monitoring, detailed activity logs, and customizable reporting dashboards that give compliance officers the operational evidence their assessments require. Multi-factor authentication and geographic access controls reduce the risk of unauthorized activity that would otherwise surface as a compliance finding. For operators managing branch networks, Currexchanger centralizes the data that makes compliance risk analysis accurate and defensible rather than theoretical. You can also use the platform's liquidity tracking tools to monitor operational exposures across currencies in real time.

FAQ

What is compliance risk assessment in simple terms?

A compliance risk assessment is a structured process that identifies where your business could violate laws or regulations, evaluates how likely and serious each violation would be, and prioritizes actions to prevent it.

How often must financial institutions conduct compliance risk assessments?

MaRisk AT 4.4.2 and EBA Guidelines require a minimum of one full assessment per year, plus additional reviews triggered by material changes in operations or regulation.

What are the most common compliance risks in financial services?

AML deficiencies, GDPR breaches, and MiFID II failures are the most frequently cited compliance risks, with penalties potentially exceeding €15 million depending on the regulatory framework and severity.

What is the difference between compliance risk assessment and a general risk assessment?

A general risk assessment covers all business risks including operational, financial, and strategic. A compliance risk assessment focuses specifically on risks arising from failure to meet legal, regulatory, and internal policy obligations.

How do you prioritize risks in a compliance risk assessment?

Risk matrices rate each identified risk by likelihood and impact, producing a critical, high, medium, or low classification. Critical risks require immediate remediation and frequent monitoring; lower-rated risks follow longer review cycles.