A transaction management system is an integrated platform that automates currency exchange operations end to end, from initiation through compliance validation to final settlement. Financial managers who understand how transaction management systems work gain a direct operational advantage: fewer manual errors, faster processing, and audit trails that satisfy regulators on demand. Modern systems combine straight-through processing (STP), real-time AML screening, and behavioral analytics into a single architecture. Currexchanger is built on exactly this model, serving currency exchange operators who manage multiple branches and face daily compliance pressure from bodies like the Anti-Money Laundering Authority (AMLA).

How transaction management systems automate the transaction management process

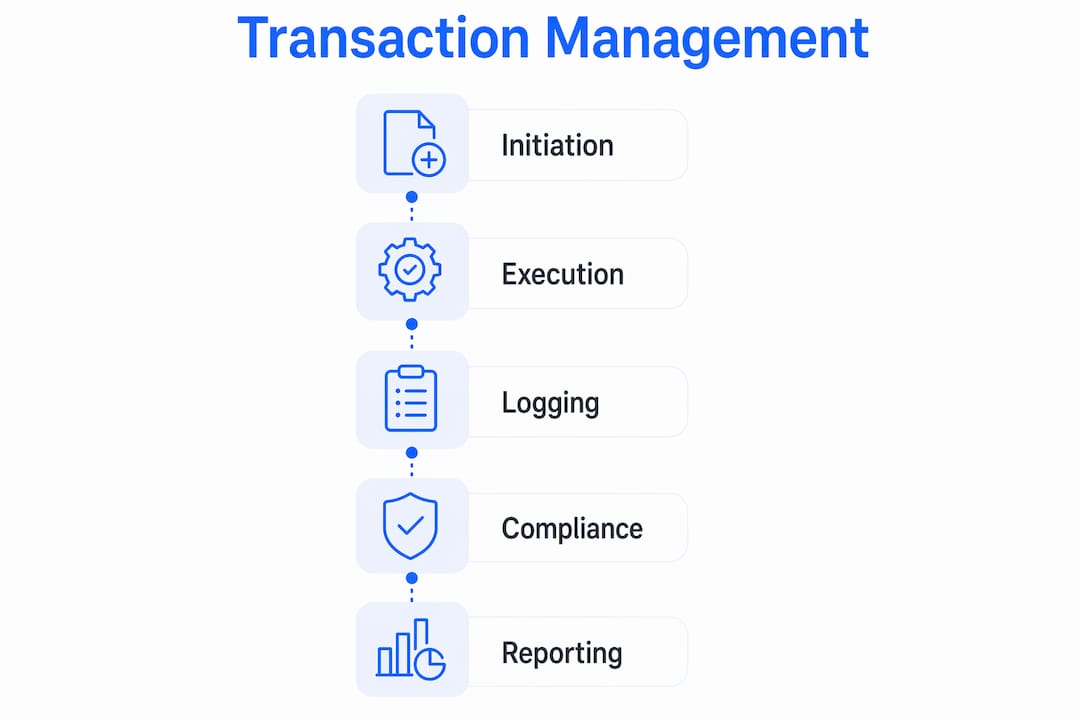

Every currency exchange transaction moves through five sequential stages: initiation, execution, logging, validation, and completion. Each stage is a decision point, and automation determines how fast and accurately the system moves through them.

- Initiation. The customer or operator submits a transaction request. The system captures counterparty identity, currency pair, amount, and timestamp in a single data record.

- Execution. The system applies the current exchange rate, checks available inventory, and reserves the required cash balance. No manual calculation is needed.

- Logging. Every action is written to an immutable ledger in real time. This record becomes the foundation for audit trails and regulatory reporting.

- Validation. The system screens the transaction against sanction lists, internal risk rules, and behavioral baselines. Low-risk transactions pass automatically through straight-through processing. Flagged transactions escalate to a compliance analyst.

- Completion. Approved transactions update cash balances, generate receipts, and trigger any required regulatory reports without operator input.

Integration with core banking APIs and external sanction lists enables continuous real-time screening and transaction contextualization at each stage. That connectivity removes the data silos that cause delays and errors in manual workflows.

Pro Tip: Map your transaction volume by risk tier before configuring STP thresholds. Setting the auto-approval limit too high exposes you to compliance gaps; setting it too low creates a bottleneck that defeats the purpose of automation.

How does real-time compliance monitoring work in transaction systems?

Compliance is not a final checkpoint. It runs in parallel with every stage of the transaction management process, and the architecture that supports it determines whether your operation can scale without regulatory risk.

Modern systems use a layered compliance approach:

- Rule-based screening. Every transaction is checked against hard rules: sanction lists, transaction amount thresholds, and jurisdiction restrictions. This layer catches clear violations instantly.

- Behavioral analytics. The system compares each transaction against the customer's established pattern. A sudden large transfer from a low-activity account triggers an alert even if the transaction passes rule-based checks.

- Sanction list checks. Regulatory frameworks require screening against financial sanction lists at least once daily, but real-time validation is standard for high-risk and cross-border transactions.

The infrastructure behind real-time monitoring matters as much as the rules themselves. Event-bus architectures like Apache Kafka allow systems to process sanction screening and behavioral analysis within seconds, not minutes. That speed is the difference between blocking a suspicious transaction before funds move and filing a report after the fact.

The EU AMLR mandates perpetual KYC to replace periodic reviews with automated continuous monitoring of client profiles and transaction patterns, effective from july 2027. Direct oversight by AMLA follows in 2028. That regulatory shift makes real-time monitoring a legal requirement, not a competitive feature. Financial managers who rely on batch screening today face a hard deadline for system upgrades.

For currency exchange operators, the 2026 AML compliance guide outlines exactly how the EU AMLR mandate reshapes transaction system design and compliance workflows.

Audit trails must also satisfy explainability requirements. Regulators do not just want to know what decision the system made. They want to know why. Systems that log decision logic alongside transaction data give compliance teams the evidence they need during inspections.

What role does behavioral analytics play in fraud detection?

Behavioral analytics is the layer of a transaction management system that learns what "normal" looks like for each customer and flags deviations. Rule-based screening catches known threats. Behavioral analytics catches novel ones.

The profiling process tracks several data dimensions:

- Transaction patterns. Frequency, average amount, currency pairs, and time of day all form a behavioral baseline for each counterparty.

- IP and device history. Transactions originating from new locations or devices receive elevated risk scores automatically.

- Counterparty profiles. The system tracks who a customer transacts with and flags new or unusual counterparty relationships.

Anomaly detection uses clustering algorithms and graph analysis to identify relationships that rule-based systems miss. A network of accounts that individually look clean but collectively show circular fund flows is a classic money laundering pattern. Graph analysis surfaces it; simple rule checks do not.

Fuzzy matching and scoring reduce false positives, which is critical when transaction volumes are high. A system that generates hundreds of false alerts per day trains compliance analysts to ignore alerts, which defeats the purpose of monitoring entirely.

Explainable AI (XAI) in AML reduces alert fatigue by enabling human analysts to understand and trust machine learning decisions during transaction monitoring. That transparency is not just operationally useful. It is increasingly a regulatory expectation.

Pro Tip: Data normalization is the unglamorous prerequisite for effective behavioral analytics. Inconsistent data formats across branches or systems produce false positives that overwhelm compliance teams. Standardize data inputs before tuning detection models.

Architectural best practices for transaction management platforms

The architecture of a transaction management system determines its long-term compliance flexibility and operational performance. Three design principles separate systems that scale from those that break under regulatory pressure.

Compliance service boundaries. Compliance service boundaries should map to regulatory domains rather than functional ones to allow independent audit and updates as regulations evolve. This design avoids full system re-certification when a single regulation changes. Each compliance domain, such as AML screening, KYC verification, or sanction checking, operates as an independently deployable service.

Distributed transaction patterns. The Saga pattern decomposes cross-service operations into independent steps with compensating transactions for rollback. This approach avoids long-lived locks and improves throughput in high-volume environments. The older two-phase commit (2PC) pattern causes performance bottlenecks and is not suited to modern transaction volumes.

Backward reconstructability. Systems must provide immutable audit trails and version-controlled decision logic to prove to regulators why transactions were allowed or blocked. This capability is not optional. It is the foundation of regulatory trust during inspections.

| Architectural approach | Key strength | Key limitation |

|---|---|---|

| Monolithic compliance engine | Simple to deploy initially | Requires full re-certification on any rule change |

| Domain-separated services | Independent audit and update per domain | Higher initial design complexity |

| Saga pattern (distributed) | High throughput, no long-lived locks | Requires careful compensation logic |

| Two-phase commit (2PC) | Strong consistency guarantees | Performance bottlenecks at scale |

| Regulatory Operating System (ROS) | Unified policy and control testing | Emerging standard; implementation varies |

Regulatory Operating Systems (ROS) unify change management, policy mapping, and control testing into a single source of truth. This trend directly addresses the compliance drift that occurs when organizations manage regulations across multiple disconnected tools. For currency exchange operators running multiple branches, a unified compliance layer is the difference between manageable regulatory change and constant firefighting.

Treating compliance as a deployment checklist rather than an architectural constraint leads to higher long-term costs and failure risks. Systems built from the start with tokenization, audit-ready data models, and clear service domains avoid the expensive retrofitting that comes when compliance is bolted on after launch.

The activity log practices used by financial systems show how integrated audit trail management supports both regulatory inspections and internal governance.

Key Takeaways

Transaction management systems deliver compliance and operational efficiency only when automation, real-time monitoring, and audit-ready architecture are built in from the start, not added later.

| Point | Details |

|---|---|

| Five-stage automation | Every transaction moves through initiation, execution, logging, validation, and completion without manual intervention. |

| Layered compliance | Rule-based screening, behavioral analytics, and sanction checks run in parallel, not in sequence. |

| Perpetual KYC deadline | EU AMLR requires continuous client monitoring from july 2027, making real-time systems a legal necessity. |

| Saga over 2PC | Distributed transaction patterns using Saga improve throughput and avoid the bottlenecks of two-phase commit. |

| Backward reconstructability | Immutable audit trails with version-controlled decision logic are required to satisfy regulatory inspections. |

Why compliance architecture is the decision that defines everything else

I have seen financial managers treat the compliance layer as something to configure after the core transaction engine is built. That sequencing is the single most expensive mistake in this space. By the time you realize your data model cannot support immutable audit trails or your service boundaries require full re-certification every time a regulation changes, you are looking at a rebuild, not a patch.

The shift to perpetual KYC under EU AMLR is the clearest signal yet that regulators expect compliance to be structural, not procedural. A system that runs batch screening overnight and calls it "monitoring" will not meet the 2027 standard. The architecture has to support event-driven processing from day one.

What I find underappreciated is the feedback loop between compliance analysts and platform owners. Analysts see the false positives. They know which alert types are noise and which carry real risk. When that knowledge does not flow back into model tuning and rule refinement, systems degrade over time even as transaction volumes grow. The best implementations I have observed treat that feedback loop as a formal process, not an informal conversation.

Explainable AI is not a luxury feature. When a regulator asks why a transaction was cleared, "the model said so" is not an answer. The system has to show its work. That requirement shapes every design decision from data ingestion to alert logging.

— Bartas

Currexchanger: built for currency exchange transaction management

Currency exchange operators face a specific version of the transaction management challenge: multiple branches, multiple currencies, and compliance obligations that vary by jurisdiction and transaction type.

Currexchanger is purpose-built for this environment. The platform covers the full transaction management process, from real-time exchange rate application and cash inventory tracking to AML/KYC compliance, document verification, and multi-branch reporting. It integrates with external AML/KYC providers and banknote verification services through API connectivity, so compliance screening runs without manual intervention. Security controls include multi-factor authentication, detailed activity logs, and geographic restrictions. Financial managers who need to manage currency exchange operations across multiple locations will find that Currexchanger handles the compliance architecture so the team can focus on the business.

FAQ

What is a transaction management system?

A transaction management system is an automated platform that handles financial transactions end to end, covering initiation, execution, compliance screening, and settlement. In currency exchange, these systems also manage exchange rate application, cash inventory, and regulatory reporting.

How does straight-through processing work in transaction systems?

Straight-through processing routes low-risk transactions through automated approval without human review. Transactions that trigger behavioral or rule-based alerts are escalated to a compliance analyst for manual assessment.

What is perpetual KYC and when does it take effect?

Perpetual KYC replaces periodic client reviews with continuous automated monitoring of transaction patterns and client profiles. The EU AMLR mandates this approach from july 2027, with AMLA oversight beginning in 2028.

Why is backward reconstructability required in transaction systems?

Regulators require transaction systems to prove why each transaction was approved or blocked. Immutable audit trails and version-controlled decision logic provide that evidence during inspections and reduce the risk of regulatory penalties.

How does the Saga pattern improve transaction system performance?

The Saga pattern breaks cross-service transactions into independent steps with compensating actions for rollback. This avoids the performance bottlenecks caused by two-phase commit and supports high-throughput processing across distributed systems.