Document verification is the process of confirming the authenticity, validity, and ownership of identification documents to meet regulatory compliance requirements and prevent financial crime. For compliance officers in financial services, this process is not optional. Regulators including the Financial Conduct Authority (FCA), the Financial Action Task Force (FATF), and the European Union's Anti-Money Laundering Directive framework treat document verification as a foundational control. Weak verification exposes institutions to enforcement action, reputational damage, and criminal liability. Understanding why document verification matters for compliance is the first step toward building a program that survives regulatory scrutiny.

Why document verification matters for compliance with KYC and AML

Document verification sits at the center of Customer Due Diligence (CDD), the process regulators require before any financial institution onboards a customer. CDD demands that institutions confirm a customer's identity using reliable, independent source documents. Without verified documents, CDD is incomplete, and the institution has no defensible basis for the risk decisions it makes.

Regulatory mandates make this explicit. The Sixth Anti-Money Laundering Directive (AMLD6), the EU's Anti-Money Laundering Regulation (AMLR), and FATF guidance all require that financial institutions collect and verify identity documents as part of their Know Your Customer (KYC) programs. These frameworks do not treat document checks as a formality. They treat them as a gatekeeping control that determines whether a customer relationship should begin at all.

The FATF 2023 mutual evaluation cycle identified weak document authentication as a primary cause of gaps in CDD, directly facilitating money laundering and sanctions evasion. That finding means regulators are actively looking for this weakness during inspections. Institutions that cannot demonstrate consistent, documented verification practices face heightened scrutiny.

"Document verification is a critical regulatory control and gatekeeper for onboarding programs to survive scrutiny from risk committees, fraud rings, and regulators. Treating it as an IT feature rather than a compliance control is one of the most common and costly mistakes financial institutions make."

The practical implication is clear. Compliance officers must ensure that document verification processes are owned by the compliance function, not delegated entirely to technology teams. The controls must be documented, tested, and reviewed as part of the institution's broader AML compliance program.

Key regulatory requirements that document verification must satisfy include:

- Confirming the customer's full legal name, date of birth, and address against government-issued documents

- Checking document authenticity features such as security markings, expiry dates, and biometric data where applicable

- Recording the verification outcome and the documents reviewed in the CDD file

- Repeating verification checks when customer risk profiles change or documents expire

What are the real consequences of inadequate document verification?

Inadequate document verification produces consequences that are financial, operational, and reputational. Compliance officers who treat document checks as a low-priority task learn this lesson through enforcement actions.

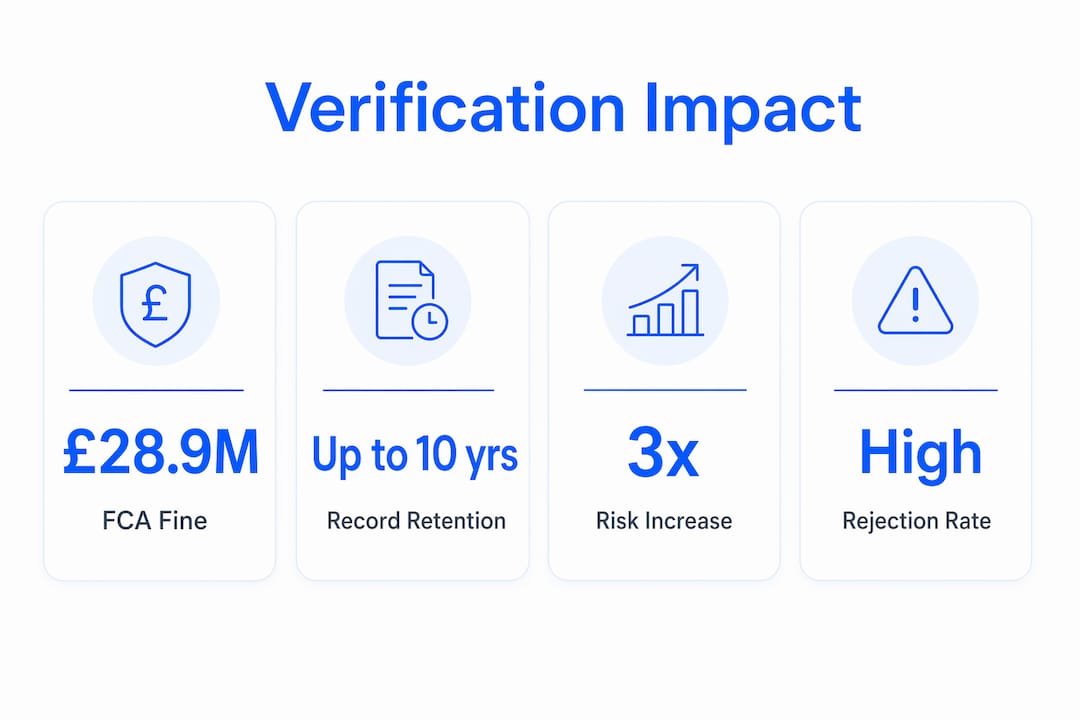

The FCA fined Starling Bank £28.9 million in 2024 for insufficient KYC controls, including inadequate document verification during rapid customer expansion. That fine illustrates a pattern regulators follow: when growth outpaces verification controls, the institution pays. Starling's case is not unique. Regulators across jurisdictions have made clear that scaling a customer base without scaling verification capacity is a compliance failure, not a business decision.

The scale of penalties extends beyond banking. A global car dealer faced $80 million in combined penalties in early 2026 for failing to manage and verify required customer documents under AML program obligations. That case matters for financial services because it confirms that AML document verification obligations apply across sectors, and regulators will pursue enforcement regardless of industry.

The operational risks of weak verification are equally serious:

- Fraud facilitation. Forged or tampered documents allow fraudsters and money launderers to establish accounts under false identities. Once inside the system, these actors are difficult to detect and remove.

- Human error in manual review. Manual document verification is subjective and prone to error, especially under high-volume conditions. Fatigue and inconsistency in manual review create gaps that fraud rings actively exploit.

- Audit failure. Regulators expect institutions to produce complete CDD files on demand. Missing or incomplete verification records make it impossible to demonstrate compliance during inspections.

- Reputational damage. Public enforcement actions, particularly those involving named institutions and specific fine amounts, damage customer trust and investor confidence in ways that outlast the penalty itself.

Pro Tip: Track your verification rejection rate by document type and channel. A sudden spike in rejections is not just a data quality problem. Reject spikes signal active fraud rings testing your controls, and they require immediate investigation, not just a process note.

How to ensure compliance through effective document verification practices

Effective document verification combines the right technology with clear process design and disciplined documentation. Neither element alone is sufficient.

Automated verification technologies

Automated document verification uses optical character recognition (OCR), artificial intelligence, and biometric matching to check documents at speed and scale. These technologies extract data from identity documents, compare it against authoritative databases, and flag anomalies that human reviewers might miss. Automated systems also apply consistent rules across every verification, removing the subjectivity that makes manual review unreliable.

The comparison below shows how manual and automated approaches differ across key compliance criteria:

| Criteria | Manual verification | Automated verification |

|---|---|---|

| Consistency | Variable; depends on reviewer | Uniform rule application every time |

| Speed | Slow under high volume | Processes documents in seconds |

| Audit trail | Often incomplete or paper-based | Digital records with timestamps |

| Fraud detection | Limited to visible forgery signs | Detects metadata anomalies and tampered fields |

| Scalability | Degrades as volume increases | Maintains performance at any volume |

Building a living CDD file

Document verification is not a point-in-time check. Regulators treat the CDD file as a living record that must be updated when customer circumstances change. CDD files and documentation must be preserved for up to 10 years after account closure, with full metadata and storage management. That requirement means institutions need document management systems that store verification outcomes, timestamps, reviewer identities, and the documents themselves in a retrievable format.

Compliance officers should build their CDD file standards around the assumption that a regulator will request any file at any time. If the file cannot be produced quickly and completely, the institution has a documentation problem regardless of how good the underlying verification was.

Common pitfalls to avoid

Compliance programs frequently fail in predictable ways. Treating document verification as a one-time onboarding step, rather than an ongoing obligation, is the most common error. Customer documents expire. Risk profiles change. A customer who passed verification at onboarding may present a different risk profile two years later. Documented root-cause analysis of verification failures proves program maturity to regulators and supports continuous improvement. Institutions that cannot explain why a verification failed, and what they did about it, look unprepared during enforcement reviews.

Pro Tip: Integrate your document verification system with your AML compliance program so that verification outcomes automatically update customer risk scores. Manual handoffs between verification and risk rating create gaps that regulators notice.

How do verification outcomes shape risk decisions and compliance strategy?

Verified document data does more than confirm identity. It feeds directly into the risk decisions that compliance officers make throughout the customer lifecycle.

Verification outcomes determine the customer's initial risk category. A customer who presents a government-issued passport with biometric data and passes liveness checks enters the relationship at a lower risk level than a customer who submits a document that triggers authenticity flags. That initial categorization drives monitoring intensity, transaction limits, and the frequency of periodic review.

Enhanced Due Diligence (EDD) triggers depend on verification quality. When a customer's documents raise concerns but do not produce an outright rejection, the compliance team must decide whether to apply EDD, request additional documentation, or decline the relationship. These decisions require clear internal policies that define what verification outcomes require which response.

Key areas where verification outcomes drive compliance decisions include:

- Risk profile assignment. Verification results feed into risk scoring models that determine monitoring thresholds and review frequency.

- EDD triggers. Partial verification failures or document anomalies must automatically escalate to enhanced review under FATF and AMLD6 standards.

- Ongoing monitoring calibration. Customers whose documents required additional scrutiny at onboarding should receive more frequent transaction monitoring. The role of activity logs in capturing these decisions is critical for audit readiness.

- Adverse action obligations. When automated verification denies onboarding, the institution has a legal obligation to explain that decision clearly to the individual. Failure to do so creates regulatory and legal exposure.

Compliance officers must also ensure that verification denial decisions are documented with the same rigor as approvals. Regulators review both. A pattern of undocumented denials raises questions about whether the institution is applying its verification standards consistently or selectively.

Key Takeaways

Document verification is a foundational compliance control that determines risk decisions, audit readiness, and regulatory defensibility across the entire customer lifecycle.

| Point | Details |

|---|---|

| Regulatory mandate | AMLD6, AMLR, and FATF require verified identity documents as a core CDD obligation. |

| Enforcement risk | The FCA fined Starling Bank £28.9M in 2024 for weak KYC and document verification controls. |

| Automation advantage | Automated verification applies consistent rules at scale, eliminating the subjectivity of manual review. |

| Living CDD files | Regulators may require access to verification records for up to 10 years after account closure. |

| Adverse action duty | Automated denials based on verification logic require clear legal explanations to avoid regulatory exposure. |

Document verification is a control, not a checkbox

I have reviewed compliance programs across financial services where document verification was buried in the IT department's backlog. The compliance team owned the policy on paper, but no one owned the outcomes in practice. That gap is where enforcement actions begin.

The institutions that handle regulatory scrutiny well share one characteristic: they treat document verification as a first-line compliance control with the same seriousness as transaction monitoring. They document failures, investigate rejection spikes, and update their CDD files when circumstances change. They do not wait for a regulator to find the gap.

The 2026 compliance environment is more demanding than it was three years ago. FATF mutual evaluations are more granular. Regulators are naming institutions and publishing fine amounts. The cost of treating document verification as a side task has never been higher. Build the control properly the first time, document everything, and make sure your technology supports the audit trail your regulators will eventually request.

— Bartas

Currexchanger's approach to compliance and document verification

Currency exchange operators face the same document verification obligations as banks, often with fewer compliance resources and tighter operational margins.

Currexchanger is built for exactly this environment. The platform integrates AML and KYC compliance controls directly into daily transaction workflows, so document verification and activity logging happen as part of normal operations rather than as separate manual steps. Compliance officers get real-time visibility into verification outcomes, audit-ready activity logs, and configurable risk controls across every branch or office location. For teams preparing for 2026 regulatory requirements, Currexchanger's compliance tools provide the documentation infrastructure that regulators expect to see. The platform also connects with external AML and KYC providers, so your existing verification technology integrates without rebuilding your program from scratch.

FAQ

What is document verification in a compliance context?

Document verification in compliance is the process of confirming that a customer's identity documents are authentic, valid, and belong to the person presenting them. It is a required component of Customer Due Diligence under KYC and AML regulations including AMLD6 and FATF guidance.

What happens if a financial institution fails document verification checks?

Regulators issue fines, require remediation programs, and in serious cases pursue criminal referrals. The FCA fined Starling Bank £28.9 million in 2024 specifically for inadequate document verification controls.

How long must institutions keep document verification records?

Regulators may require access to CDD files, including document verification records, for up to 10 years after account closure. Institutions need document management systems that store these records with full metadata and retrieval capability.

What triggers Enhanced Due Diligence in document verification?

Document anomalies, partial verification failures, or high-risk customer profiles trigger EDD under FATF and AMLD6 standards. Compliance teams must define clear internal policies that specify which verification outcomes require enhanced review.

Can institutions deny onboarding based on automated document verification?

Yes, but they must provide a clear legal explanation to the individual when an automated verification decision results in denial. Failure to explain adverse action decisions creates regulatory and legal exposure for the institution.